The trade summary is used to record the name of your trade, period of accounts together with a summary of any lossed.

Add the Trading profits section to the return (or select it if already added), then select the Trade Summary tab.

Complete the section as follows, then select Save changes.

Trade

If the trading name is different from the company name, enter the correct trading name here.

Select if the qualifying activity has ceased in this period. This is normally selected for the accounting period during which the company ceases trading. This ensures that balancing capital allowances on pools are correctly calculated.

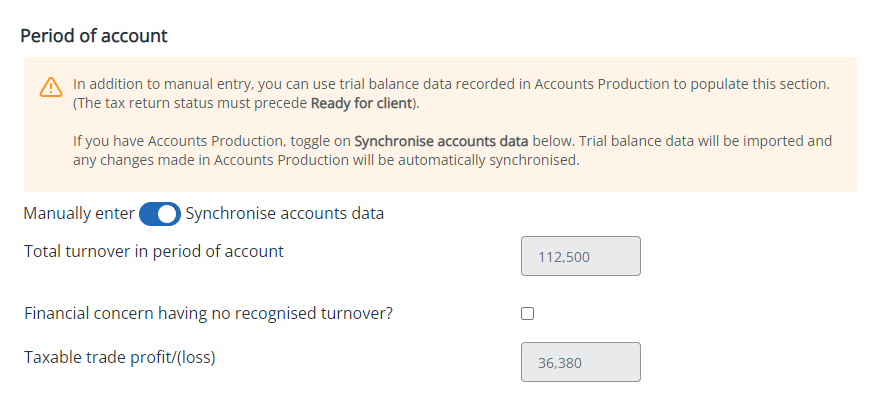

Period of account

If the period of account is different from the accounting period, you can enter the correct period of account by selecting Change. Where a long period of account is entered, you can apportion figures automatically from the long period to the accounting period.

In addition to manual entry, you can use trial balance data recorded in IRIS Elements Accounts Production to populate this section. (The tax return status must precede Ready for client).

If you want to synchronise accounts data, toggle on Synchronise accounts data. The trial balance data will be imported and any changes made in IRIS Elements Accounts ProductionAccounts Production will be automatically synchronised.

Displays the start date of the period of account. This field is only visible if the period of account is different from the accounting period.

Displays the end date of the period of account. This field is only visible if the period of account is different from the accounting period.

Enter the total turnover in the period of account.

Select if there is no recognised turnover in the period of account.

Shows the taxable trading profit or loss as calculated on the Adjustments to trade profit tab.

Only shown when the period of account differs from the accounting period and you have chosen to automatically apportion profits. This field shows the trading profits apportioned to the current tax return.

Trading losses summary

Enter all losses as positive figures.

Enter the trading losses brought forward from previous periods, if any.

Under new s279ZZ CTA 2010, if a company wishes to set brought forward losses against profits arising from 1 April 2017, they are required to specify the amount of their deduction allowance in their corporation tax return for the period. Please attach a PDF to the tax return stating the amount of the allowance. For additional information please see HMRC.

Enter the brought forward losses that are used to reduce profits of the current year.

Enter the total of any losses brought back from a later period under s37(3)(b) or s39(2).

Enter the total losses used to reduce other income and gains in this accounting period.

Shows any loss surrendered to other group companies (from the Group Relief section).

Shows any loss that is surrendered for R & D tax credit. This field will only be shown if a claim is made for R & D tax credit.

Shows any loss that is surrendered for film tax credit. This field will only be shown if a claim is made for film tax credit.

Shows any unused trading losses that are being carried forward.

Shows any unused trading losses that are being carried forward.