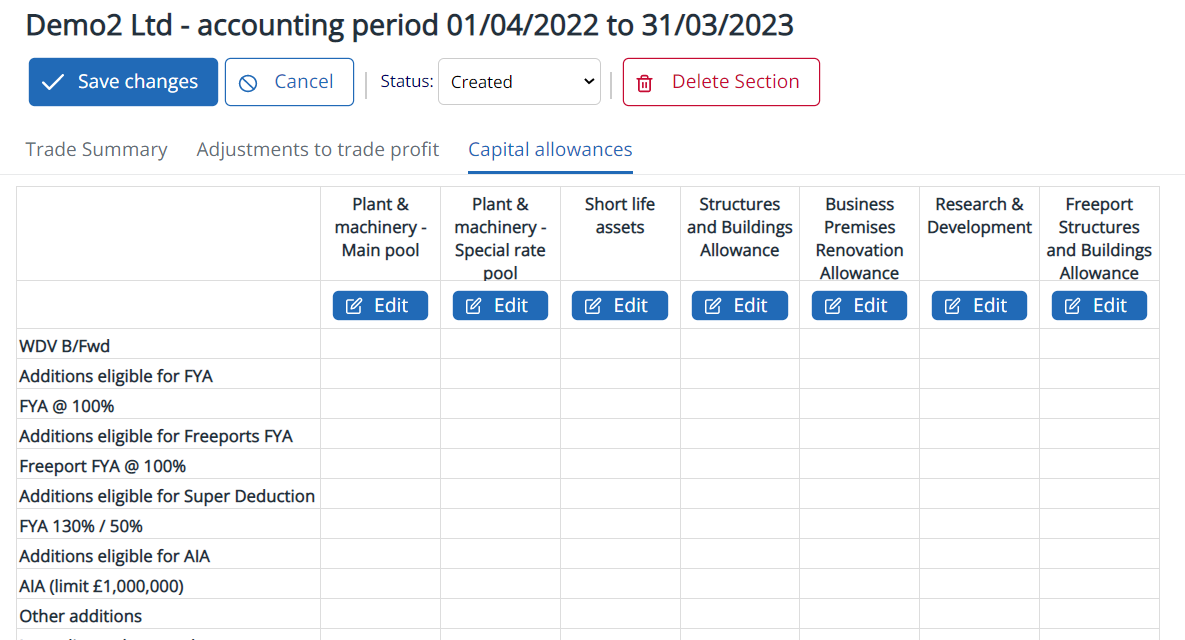

The Capital allowances tab is used to record the various types of capital allowance.

Add the Trading profits section to the return (or select it if already added), then select the Capital allowances tab tab.

For each type of asset, the grid shows a summary with each asset type in its own column. To access the input area for an asset type, select Edit at the top of the column for that type.

Depending upon the period dates some asset types may not be available. Where the period is not for a full 12 months the capital allowances will be assigned on a pro rata basis.

Below the button, the following information is summarised for each asset type:

The sum of the expenditure in the period that is eligible for 100% First Year Allowances.

The amount of 100% First Year Allowance claimed on the relevant expenditure.

The sum of the expenditure qualifying for Super Deduction and Special Rate allowances for the period 1/4/2021 to 31/3/2023.

The total Super Deduction and special rate allowances being claimed on the relevant expenditure.

The total expenditure in the period that is eligible for the Annual Investment Allowance. This may be more than the AIA limit for the year.

The Annual Investment Allowance claimed. The title for this row also shows the maximum amount of AIA that can be claimed in the period, assuming that the AIA limits are not shared with another business.

The total expenditure in the period that is not eligible for First Year Allowances or Annual Investment Allowance.

The value of all asset disposals in the accounting period.

Any balancing allowance or balancing charge that is applicable for the asset type.

The balancing charges calculated as arising on Super Deduction and special Rate expenditure

The residue of expenditure after adding the written down value and additions, and after deducting FYA and AIA claimed and disposal proceeds. This is the amount on which writing down allowances can be claimed.

For asset pools this line will indicate the writing down of the remaining pool balance where the balance of the pool is less than the small pools limit for the period.

The maximum writing down allowance that can be claimed in the period. The rates for writing down allowance will be different for different types of asset.

The total writing down allowance not actually claimed for the asset. This figure will reduce the WDA claim and increase the written down value carried forward.

For plant and machinery pools, the value of any assets transferred into or out of the pool at the end of the period.

The written down value of the assets to be carried forward to the next accounting period.

The sum of all allowances claimed for each type of asset; this includes First Year Allowance, Annual Investment Allowance, Balancing allowances/(charges) and WDA claimed.

Private use is not applicable for companies. Private use must be accounted for as a Benefit in Kind for the employee or director