Capitalising an Asset

Capitalisation is the addition to the Balance Sheet of an Asset that could otherwise have been treated as an Expense. In general, the capitalisation of an Expense is used in relation to the acquisition of a new Asset that is a long-term cost, rather than an expense for only one year, and where the cost will be spread out over a specific period of time.

Given the complexities surrounding Academy Fixed Assets, assuming the Assets are sat within the expenditure nominal, there are a couple of adjustments required.

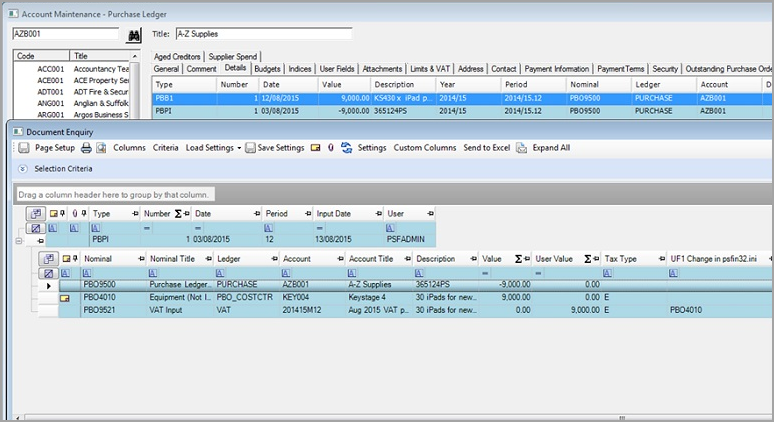

In this example, PBPI 1 has been posted to the PBO4010 expenditure nominal and needs to be converted to an asset on the balance sheet.

Adjustment 1 – Move the Expenditure to the Balance Sheet

The first adjustment is to post a General Journal crediting the Cost Centre used for the purchase and debiting the Fixed Asset at Cost Nominal ( nominal.

You will need to set up a fixed asset account in order to post the journal. See Adding a New Fixed Asset.htm

The expenditure has now been moved to the fixed asset account defined in the journal.

Adjustment 2 – Transfer the funds from Revenue to Capital

For the second adjustment, post a General Journal debiting the Cost Centre used for the purchase via the

The credit value of £9,000 posted to the

There is also a credit entry against the Capital Ledger Account