Overview of VAT

What is VAT?

VAT is a sales tax charged by business on certain goods and services they provide. When a business is subject to VAT it is added to their invoices, which is then paid to HMRC.

In addition, the business can deduct the VAT they have paid in making their vatable sales from the payment to HMRC, i.e. only the net VAT amount is paid to HMRC.

From 1st April 2011, a new VAT refund scheme was introduced for academies/MATs enabling them to reclaim the VAT incurred on purchases, imports, and acquisitions relating to their non-business activities. These are predominantly the provision of free education, together with goods and services closely related to this, which are sold at or below cost price for the direct use of pupils.

VAT Related Terminology

The following terms are used in relation to VAT:

|

Term |

DESCRIPTION |

|

Input VAT |

VAT on purchases made by the academy/MAT for incoming goods/services. Input VAT can only be recovered where:

|

|

Output VAT |

VAT on sales made by the academy/MAT for outgoing goods/services. Output VAT can only be charged by an academy/MAT if they are registered for VAT. |

|

Standard Rate |

The standard rate of output VAT is 20%. Input VAT is recoverable on purchases that include the standard rate of VAT, such as computers and office equipment. |

|

Reduced Rate |

The reduced rate of output VAT is chargeable at 5%. Input VAT is recoverable on purchases that include the reduced rate of VAT, such as energy saving materials and domestic fuel. |

|

Zero Rate |

Zero rated suppliers are taxable but at a rate of 0%. This means VAT is not charged to the customer, but the VAT incurred in making the supply can be recovered. Examples include books, children’s clothing and footwear, certain foods, etc. |

|

Exempt |

No VAT is chargeable, but equally, no VAT can be claimed. |

|

Outside the scope |

No output or input VAT is payable under any circumstance. A transaction is outside the scope if it is:

For example: Wages payments and fees fixed by law (congestion charge, MOT, etc). |

|

Recovering VAT |

The procedure by which a VAT registered academy/MAT can recover the VAT it incurs on purchases that are used to make taxable supplies. |

|

Reclaiming VAT |

The procedure by which an academy/MAT can obtain a refund (under the S33b scheme) for the VAT it incurs on purchase that are used in its non-business activities. Both VAT registered and unregistered academies/MATs can obtain VAT refunds under the scheme. |

|

Directly Attributable |

VAT on a purchase is directly attributable to an activity type (taxable, exempt or non-business) if the purchase is used wholly in that type of activity. For example, the hire of an agency teacher by an academy/MAT to provide non-business education will be directly attributable to the academy/MAT’s non-business activity. |

|

Residual VAT |

VAT on a purchase is residual if it is to be used for different activity types. Typically, where there is mix of different types of activity, VAT on overheads will be residual. For example, if an academy provides non-business education, but also lets out rooms on a business basis, then VAT on shared gas and electricity costs will be residual. |

|

De-minimis |

A VAT registered business cannot normally recover the VAT it incurs in its exempt activities. However, if the overall level of exempt activity is very small, both in absolute terms and in comparison, to the level of taxable activity, then the VAT incurred in exempt activities can be recovered. In this situation the exempt activity is said to be ‘de-minimis’. |

When Should an Academy/MAT Register for VAT?

VAT registration is required when VAT taxable turnover reaches the set threshold (this is currently £83,000 at the time of publication but should be checked on the HMRC website). The VAT taxable turnover includes the value of any goods or services supplied within the UK, unless they are exempt from, or outside the scope of, VAT therefore it includes any supplies that are standard and zero-rated.

What Should an Academy/MAT do?

The first step is to identify the academy/MAT’s supplies and establish which category they fall into (standard rated, exempt, zero rated or outside the scope).

It is then necessary to calculate the VAT taxable turnover to determine whether the current threshold has been exceeded, requiring the academy/MAT to register for VAT.

If the taxable turnover is below the current threshold, you should consider whether it would be beneficial to register for VAT on a voluntary basis. If VAT registration is not required or beneficial, or not possible due to the lack of any taxable business supplies, you should use form VAT 126.

Regardless of which mechanism is used, all academies/MATs should maintain systems and processes for retaining the relevant accounting records to support their VAT claims and returns. Academies/MATs need to be able to make these available to HMRC on request.

The IRIS Financials system records VAT and can be used to produce either a VAT 100 Return (for VAT registered academies/MATs) or a VAT 126 return (for academies/MATs not registered for VAT).

VAT returns are produced either monthly or quarterly depending on the requirements of the academy/MAT.

If your VAT Periods are set up monthly, if you send your VAT return to HMRC using our VAT Returns MTD module, you must submit your returns at the same frequency as your VAT periods, i.e. monthly for monthly VAT periods, quarterly for quarterly VAT periods.

What Costs can be Reclaimed?

The costs that can be reclaimed depend on whether the academy/MAT is VAT registered and what business activities (if any) are carried out.

Academies/MATs not Registered for VAT

Only VAT incurred on costs and expenses linked to non-business activities can be reclaimed - such as costs incurred in providing free education, or in receiving grant funding/voluntary donations where nothing is supplied to the funding body/donors in return.

Academies/MATs Registered for VAT

As for non-registered academies/MATs, VAT on costs incurred in order to educate the pupils (non-business activities) can be reclaimed. VAT costs incurred in relation to the provision of taxable business supplies - whether VAT is charged at the standard or zero rate - can also be reclaimed.

Where a number of academies are run by a single trust, the trust is the legal entity required to register for VAT. The implications are that in most cases, there is a single VAT return, one partial exemption calculation and an increased chance that taxable supplies will exceed the VAT registration threshold. In a very few cases, each academy could continue to submit a VAT 126 form currently.

Transactions between participating academies within the MAT can be ignored as intra VAT registration transactions.

VAT costs incurred in the provision of exempt supplies generally cannot be reclaimed, unless the amount is below certain de-minimis limits. This can mean that academies need to apply a partial exemption method in order to calculate the proportion of VAT on their costs that is allocated to exempt activities.

This can occur within a MAT where two or more schools operate a sports centre, for example, which has both taxable and exempt lettings. Additionally, the sports centre could also be used for non-business activities in education.

Partial exemption attribution is likely to be more challenging, given the makeup of each MAT, so thought to agreeing a special method should be considered.

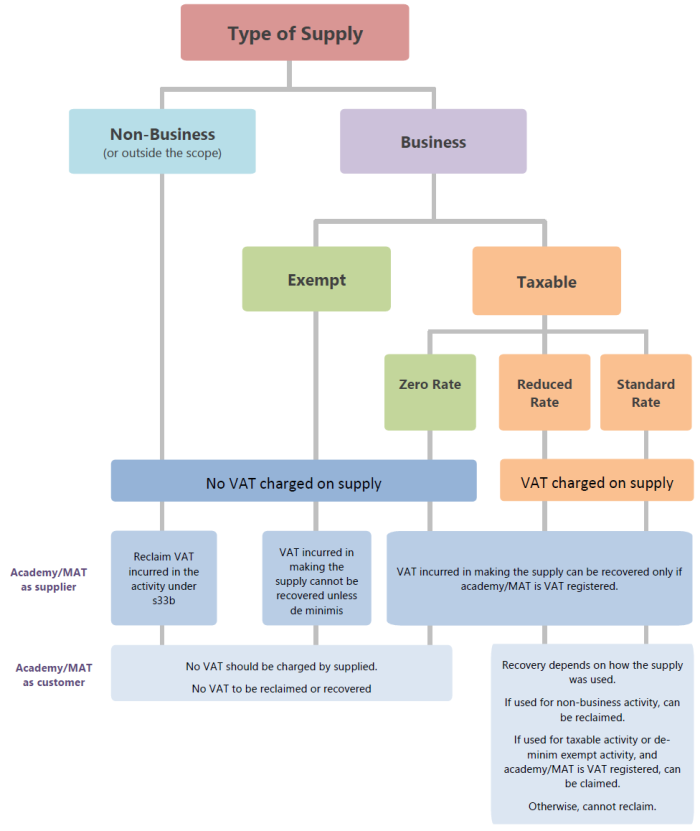

Understanding how Activities are Classified for VAT

For the purposes of VAT, it is important to understand how activities are classified. There is no prescribed method, and your establishment/organisation may use a different approach. The following description and chart provide a typical example.

Business Activities - for VAT purposes, business means any continuing activity/supply which is 'in the course of furtherance of business'. These can include charitable and not for profit activities. There are two key considerations:

-

Whether the activity mainly involves the making of supplies for a charge.

-

Whether a supply of goods or services is made which is comparable with, and/or in competition with, supplies made by the private sector.

Taxable Business Activities - all business activities, except those that are exempt or non-business are taxable supplies. If you are registered for VAT, then all the taxable business transactions that are liable for VAT are called taxable supplies. They are either standard rated, lower rated, or zero rated.

Exempt Business Activities - are business transactions that are outside the scope of the UK VAT system therefore VAT is not chargeable at either the standard or zero rates.

Non-Business Activities (outside the scope) - These are activities that do not fall under the business definition, are made by someone who is not a taxable person, and are not made in the course of furtherance of business. For example, an establishment/organisation providing free advice to its members.

Please refer to the following table to determine the type of activity and how it could be treated for VAT purposes. Please seek professional advice on how each activity should be treated in relation to VAT as required.

|

Income Stream |

ACTIVITY |

VAT Treatment |

|

GAG Funding |

Non-business |

Outside the scope (X) |

|

Donations (where freely given) |

Non-business |

Outside the scope (X) |

|

Educational school trips provided at or below cost |

Non-business |

Outside the scope (X) |

|

Fees for education |

Business |

Exempt (E) |

|

Items for use in the classroom provided at or below cost e.g. calculators, stationery, laptop, musical instrument |

Non-business |

Outside the scope (X) |

|

Transport from home to school |

Non-business |

Outside the scope (X) |

|

After school and breakfast clubs (8.00am to 6.00pm) at or below cost |

Non-business |

Outside the scope (X) |

|

Car parking for the general public |

Business |

Standard rated (S20) |

|

Catering for pupils (including tuck shops) at or below cost |

Non-business |

Outside the scope (X) |

|

Catering for pupils run for a profit |

Business |

Standard rated (S20) |

|

Catering for non-pupils (including teachers) |

Business |

Standard rated (S20) |

|

Vending Machines |

Business |

Standard rated (S20) |

|

Commissions from photographers |

Business |

Standard rated (S20) |

|

Events e.g. proms, admission to musical, theatrical performance |

Business |

Standard rated (S20) |

|

Fundraising events |

Business |

Exempt (providing certain conditions are met) (E) |

|

Sale of school uniforms |

Business |

Zero rated for sizes up to 14 years old, otherwise, standard rated (Z) |

|

Sale of photographs to students |

Business |

Standard rated (S20) |

|

Sale of printed matter |

Business |

Zero rated (Z) |

|

School merchandise |

Business |

Standard rated (S20) |

|

Nurseries / Holiday clubs when a fee is payable |

Business |

Exempt (E) |

|

Student accommodation at or below cost |

Non-business |

Outside the scope (X) |

|

Student accommodation run for a profit |

Business |

Exempt (E) |

|

Room hire |

Business |

Exempt unless opted to tax (E) |

|

Letting of sports facilities to other schools, clubs, associations etc. |

Business |

Exempt if the 24 hour/series of lets conditions are met, otherwise, standard rated (E) |

|

Provision of sports facilities / services to individuals |

Business |

Exempt (E) |

|

Supply of staff to other charities (and staff member engaged only in non-business activities at both the provider and recipient) |

Non-business |

Outside the scope (X) |

|

Supply of teaching staff to another academy |

Business |

Exempt (E) |

|

Secondment of general staff |

Business |

Standard rated (S20) |

|

Consultancy services |

Business |

Standard rated (S20) |

|

Sale of sports equipment |

Business |

Standard rated (S20) |

Activities by Month

The following list provides some suggested VAT activities that can be carried out at various times during the financial year.

|

MONTH |

ACTIVITY |

|

July |

VAT elements are automatically posted to correct VAT periods when a document is posted to Books. It is therefore essential that you check what VAT periods are currently available and add periods for the new financial year if required. |

|

August |

Check that VAT periods balance to zero. Open the new VAT period. |

|

September |

Carry out your final VAT return. Submit your VAT claim for August. |

|

September to November |

Finalise VAT claims for last year. If you still have unclaimed VAT for the old year, you can either run your VAT return before closing the year or, if your VAT return cycle means that you need to claim this in the new year, run the old year return and merge its results with the first new year return. Close any VAT periods no longer required – close any VAT periods that you want to prevent users from posting VAT into. This can be done even if the VAT return has not been submitted. |