|

|

|

|

If the cash basis is no longer to be used when computing profession or vocation profits, certain profits that would escape tax because of the change of basis will be subject to a catch-up charge. The charge is payable over either ten or six years.

The screen is the same for both sole traders and partnerships.

Select Trade, Profession and Vocation | Sole Trade or Partnership | double-click on the account period and click the Adjustments, Losses, Overlap and Tax tab.

Click the magnifying glass next to Adjustment on the withdrawal of cash basis.

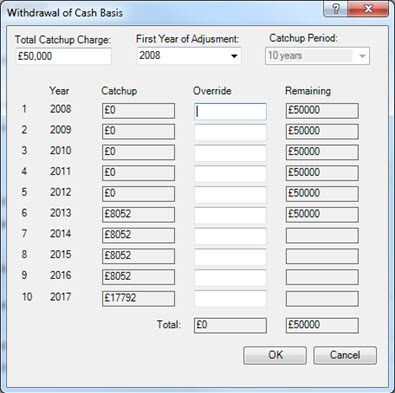

The following screen displays:

Select Trade, Profession and Vocation | Sole Trade or Partnership | double-click on the account period.

Click the Trading Income tab and the click the magnifying glass next to Adjustment on the withdrawal of cash basis.

The following screen displays.

Total Catchup Charge - enter the total catch-up.

First Year of Adjustment -select the first year in which the catch-up charge will be taxed from the drop-down list. The total will be charged to tax in 10 instalments over the tax years that follow.

Catchup Period - pre-2014 this will be 10 years. From 2014 onwards, select the number of years from the drop-down list.

Catchup - the catchup charge is automatically calculated at 10% (for a catchup period of 10 years) and 1/6th (for a catchup period of 6 years) of the original total adjustment and displays it in this column.

Override - enter the amount to be charged to tax in the tax year. This amount may not be 10% or 1/6th of the catch-up charge if:

the trader has elected to be charged on more than the minimum instalment

chargeable profits are lower than the catch-up charge in which case the amount charged to tax may be capped to be 10% of the chargeable profits