|

|

|

|

To access Loans to Participator in IRIS Business Tax:

Loans to Participators can only be access for limited company clients.

This is integrated with IRIS Accounts Production and the movement in Director Current Account (less than a year) forms part of the data entry process.

For further detailed analysis of the balance b/f and the new loans outstanding turn to examples listed on page 3 onwards.

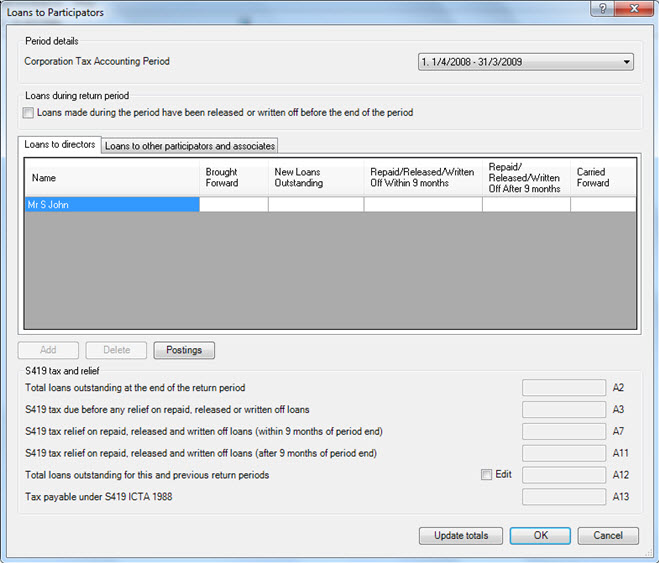

Loans during return period - select this option if there were any loans made during the period that have been released, or written off before the end of the period. This is used to complete box A1 on the CT600A.

Corporation Tax Accounting Period - select the relevant CTAP where there are more than one CTAPs.

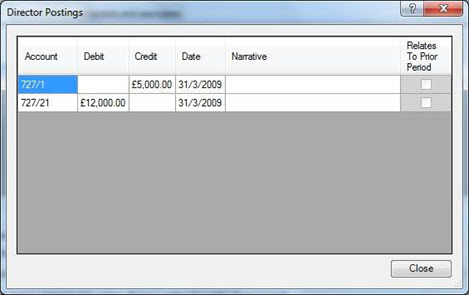

Postings - click this option to see postings being posted in Accounts Production against account code 727 and 728.

Loans to other participators and associates - click this tab if you have loans made to other participators and other associates for the relevant period.

CT600A boxes - box A2; A3; A7; A11; A12; and A13 are the corresponding boxes on the CT600A.

Box A2 - total loans within S419 ICTA 1988 made during the return period which have not been repaid, released or written off before the end of the period.

Box A3 - Box A2 multiplied by 25%.

Box A7 - (total amount of loans made during the return period which have been repaid, released or written off after the end of the period but earlier than nine months and day after the end of the period) multiplied by 25% equates to ‘’Relief due for loans repaid, released or written off after the end of the period but earlier than nine months and one day after the end of the period.’’

Box A11 - (total amount of loans made during the return period which have been repaid, released, or written off more than nine months after the end of the period and relief is due now) multiplied by 25% equates to ‘’ Relief due now for loans repaid, released or written off more than nine months after the end of the period.’’

Box A12 - total of all loans outstanding at end of return period - including all loans outstanding at the end of the return period, whether they were made in this period or an earlier one.

Box A13 - tax payable under S419 ICTA 1988; this is box A3 minus total of boxes A7 & A11.

The calculations of New Loans outstanding takes into account the account code 727 & 728 in Accounts Production. In the event where the reconciliation of the account code 727 & 728 gives rise to a debit balance a New Loans Outstanding which may give rise to s419 tax due.

727/1*1 Director 1 5000 credit

727/2*1 Director 1 2000 credit

Expected result - in this situation there is as an overall credit balance of 7000 therefore the loans to participators screen will not show any loan outstanding.

727/1*1 Director 1 5000 debit

727/2*1 Director 1 2000 credit

Expected result - in this situation there is as an overall credit balance of 2000 therefore the loans to participators screen will not show any loan outstanding.

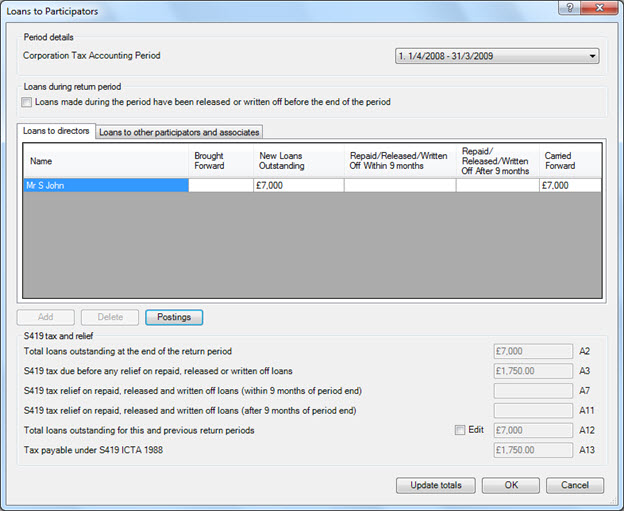

727/1*1 Director 1 5000 credit

727/21*1 Director 1 12000 debit

Expected result - in this situation there is as an overall debit balance of 5000 and the loans to participators screen will show a loan outstanding of 7000 for the director.

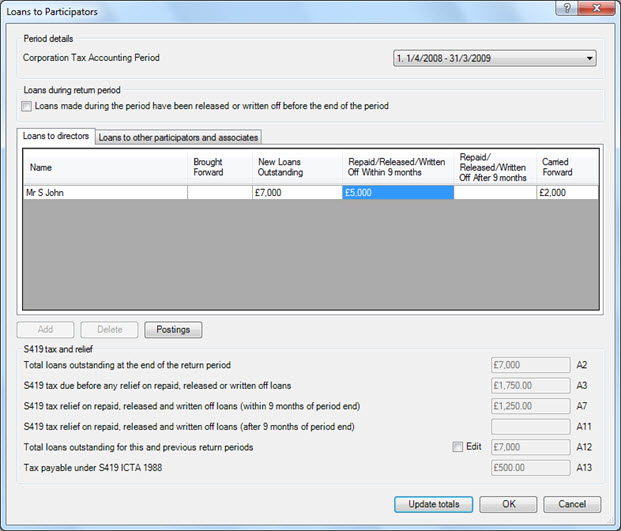

The illustration below shows how this would appear on various screens in IRIS Business Tax.

The screen shows that there is an overall balance of £7,000 from the Accounts Production Account Code 727/1 and 727/21.

You can click Postings which will show you the entries in Accounts Production for a particular director.

Figure 1

The screen shows entries that would appear

on the CT600A:

Figure 2

727/2*1 Director 1 2000 debit

Expected result - in this situation there is as an overall debit balance of 2000 and the loans to participators screen will show a loan outstanding of 2000 for the director.

727/1*1 Director A 800 credit

727/2*1 Director A 12000 credit

727/21*1 Director A 7000 debit

Expected result - in this situation there is as an overall credit balance of 5,800 therefore the loans to participators screen will not show any loan outstanding.

You are required to enter the repayment/ write off relating to the ‘Loan

Outstanding’ when directors put money into the company’s bank account

or the company crediting the director’s loan account with a payment, for

example a dividend, salary or bonus. Or it could have been simply written

off.

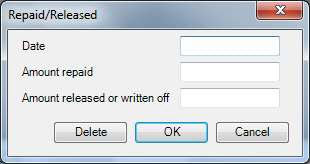

To enter amount repaid/ released/ written off against ‘Loan outstanding’ you are simply required to double-click onto the box repaid/ released/ written off within 9 months or after 9 months whichever one is relevant.

Once you double-click onto the box the following box displays.

Simply enter the required information and click OK.

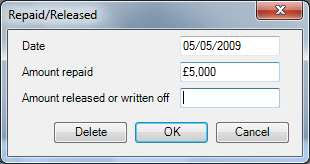

Figure 1 above shows £7,000 loans outstanding for year end 31/03/2009. For example, £5,000 of this was repaid by the director on the 05/05/2009 which is earlier than 9 months and one day before the account period end date.

Once this information has been entered the Figure 1 would reflect this change accordingly.

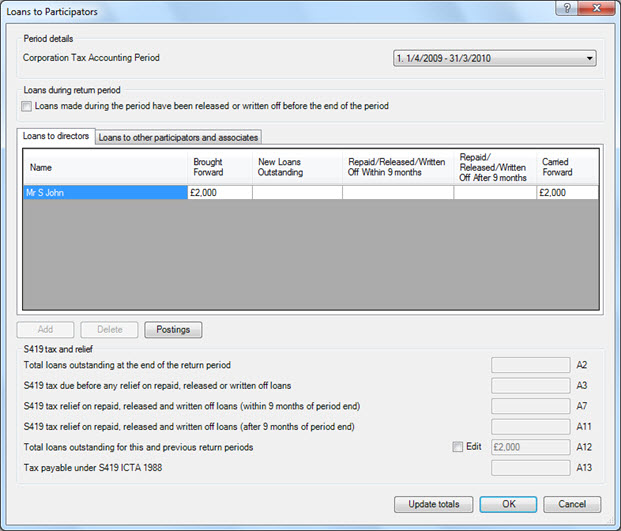

Screen below (Figure 3) shows the revised position based on the payment has been entered.

Carried forward figure has been changed to £2000 as well as the boxes on the CT600A towards the bottom of the screen.

This information will be carried forward to the next account period, that is, 31/03/2010 upon a ‘bring forward’ in the following year. Fig 4 shows the brought forward balance for the year end 31/03/2010.

If you require to enter in a repayment for a loan that has been brought forward then you would have to go back to the year that the loan was taken out and put the payment in.

The brought forward amount in the CTAP that

you are working on (not the one that you have just entered the payment

on) will then have to change so that the carried forward amount changes

to the correct figure that is still outstanding.

To do this:

Select the current CTAP and go to Data Entry | Loans to Participators

Highlight the brought forward figure and select Override

Put in the correct figure and click OK.

Figure 3

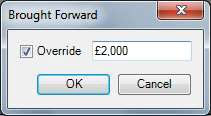

The screen below shows the brought forward balance into 31/03/2010 being £2,000 following a ‘bring forward’. Bring forward can be done by going into Edit | Bring Forward.

If a payment has been made towards this b/f balance of £2,000 users are required to go back to the previous year and enter paid/ released/ written off details and submit an amended return with the revised details. Users are also required to ‘Bring Forward’ in the following year so that the revised details appear under the Loans to Participator screen.

More information about making a payment towards the loans and useful information about Loans to Participators can be obtained by clicking here

Figure 4

It is possible to override a balance brought forward and new loans outstanding by simply double-clicking onto the fields i.e. Figure 4 £2,000 or empty box below new loans outstanding.

On the following screen select Override

and simply enter the amount and click OK.

Once users have to click onto OK and then click Update Total to update

CT600A boxes.