How to carry back trading losses for a Limited company in Business

Tax

Introduction

This topic explains the necessary steps for carrying back losses for

a limited company. This process involves a number of entries which are

detailed below.

Loss making period

Enter losses to carry back.

Indicate on the CT600 that Repayment

is due for an earlier period.

Previous years where the loss would be carried back to if an amended

return is being sent

Indicate on the CT600 that Repayment

is due for this return period.

Enter losses brought back for each

of the years with the amount relevant to each year/s.

Enter amount of ‘tax already been

paid but (not already repaid)’ in box 91for each of the years with

the amount relevant to each year/s.

Send an amended return for each of

the years where loss has been carried back to.

Loss arising period

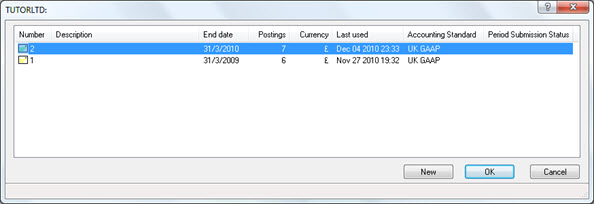

- Select the period ( for example, posting file) when the losses

arose. To select the period click the magnifying glass next to the

company identifier.

In the example below; 31/03/2010 is the loss

arising period and losses would be carried back to period ending 31/03/2009.

- Highlight the period and click OK.

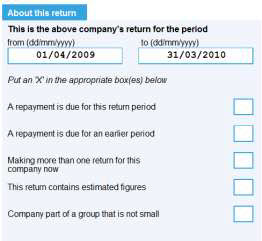

- Once the loss making period has been selected, select the A repayment is due for an earlier period

option on page one of the CT600 under the section About

this Return.

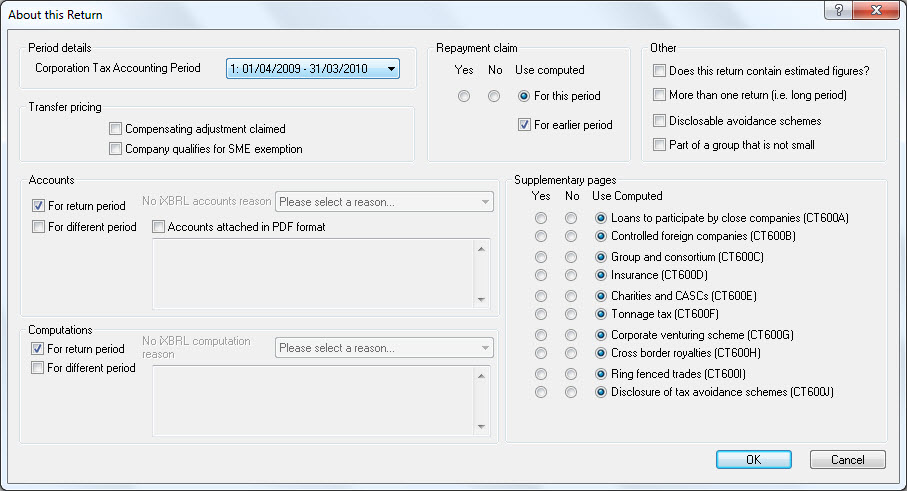

This box can be ticked by going to Data Entry | Summary

and as indicated on the screen below, selecting the For

earlier period option.

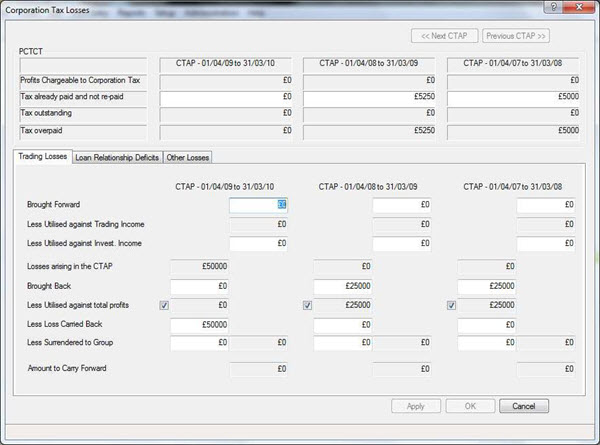

- Once the above option has been selected go to Edit

| Losses

Users are required to make an entry in the box Loss Carried

back in the loss making period. In our example, £50000

was entered in Less Loss Carried

Back.

- Enter how much of the losses you would like to be brought back

for each of the relevant CTAP column. In the example we have brought

back £25000 into period ending

31/03/2009 and the remainder £25000

into period ending 31/03/2008, reducing each of the periods profits

to nil. This entry will appear on the corporation tax computation

and in box 30 of the CT600.

Box 31 will also be selected

automatically.

- Enter Tax already paid

(but not already repaid) in row marked ‘c’. In the example two entries

have been made each equal to the amount Tax outstanding before the

losses were brought back. Notice once the entries have been made IRIS

automatically updates ‘Tax Overpaid’ row. The entries will be appearing

on the corporation tax computations as well as the relevant sections

of the CT600 accordingly.

- Last step of the process is to select the Repayment

is due for this return period option which will be selected

automatically by IRIS Business Tax for the relevant periods provided

there is an entry on 141 and/or 142 of the CT600.

- Send an amended return for all the earlier periods with losses

brought back. If you do not wish to send in an amended return for

the previous year’s then you can go to edit/notes and put a note in

to advise the HMRC that the losses have been carried back to 2009

and 2008 and that you are attaching the previous year’s computations

and CT600’s to show the repayments due.

You can then produce a pdf computation for the previous years and a

pdf ct600 for the previous years and attach them to the electronic

tax return of this year.