|

|

|

|

Limited company clients may qualify to claim relief on the expenditure incurred on research and development. This topic explains the details of entries that would be required on the CT600 and computation as per HMRC guidance.

Click the links below to jump to a particular section:

Step 1 - Business Size

Step 2 - Entering the R & D Expenditure

Step 3 - Entering the Tax Credit

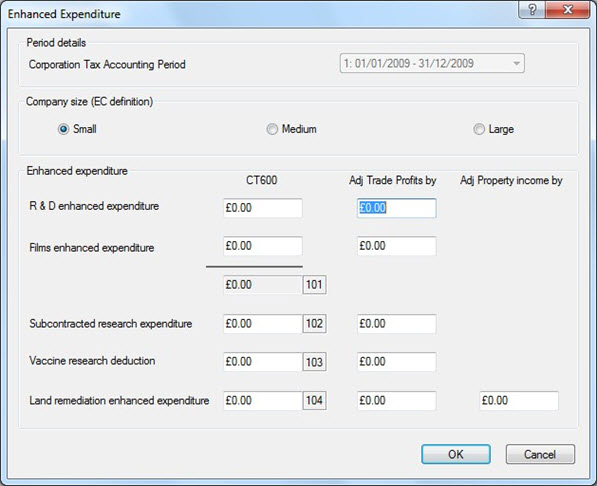

Users are required to select the size of the business.

This is essential as the amount you are able to claim will vary with the size of the company. This will also put a X in either box 99 (SME) or box 100 (large companies).

There may be an additional option, Input Enhanced Expenditure, if the account period straddles over 01/08/2008 and the rates are different.

In the screen above the entries would be as follows:-

For a SME company you would

put 175% of the enhanced expenditure

into the CT600 box and in the

Adj Trade Profits by field you

would put in 75%, then click OK.

For a large company you would put 130% of the enhanced expenditure into the CT600 box and in the Adj Trade Profits by you would put in 30%, then click OK.

Click Reports then Corporation Tax and select Basic. You will see that the adjusted by amount is showing in the computation. If the company has made a loss then they would be able to claim tax credit (step 3 below), if the company has made a profit then no tax credit can be claimed.

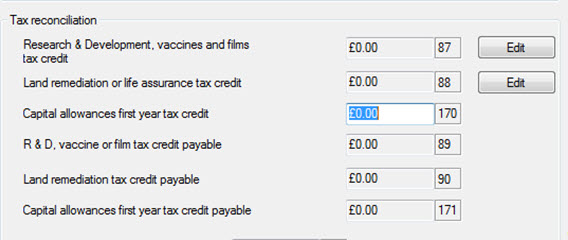

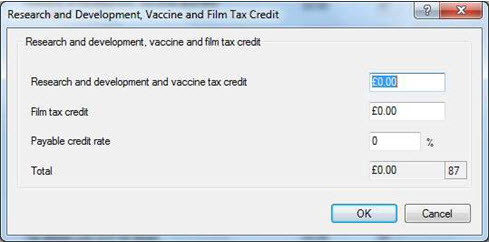

If the limited company or organisation is a SME and you need to convert some or all of the tax relief into payable tax credits, users are required to put the amount payable in box 87.

Click Data Entry, Calculation then Tax Reconciliation.

Click Edit next to box 87.

Enter the required figures and click OK.

For expenditure incurred on or after 1 August 2008 the amount of payable tax credit that a company is entitled to for an accounting period is the lesser of:

14% of the surrenderable loss for that period;

14% of the 175% R&D deduction

The company’s PAYE and NIC liabilities for the payment periods ending in that accounting period.

If you are required to put an X in the repayment due for this return period box on page 1:

Click Data Entry then Summary.

Under Repayment Claim select the For earlier period option and click OK.

Useful information about rates:

https://www.hmrc.gov.uk/ct/forms-rates/claims/randd.htm

https://www.hmrc.gov.uk/manuals/cirdmanual/CIRD80250.htm